As of April 1, 2026, several significant changes to the Indian income tax landscape have come into effect. These updates, largely driven by the Income Tax Act, 2025, aim to simplify compliance and offer more relief to small taxpayers.

New Tax Regime slabs that are now the default for the 2026-27 tax year.

1. The New “Tax Year” Concept

The traditional concepts of “Previous Year” (FY) and “Assessment Year” (AY) have been replaced by a single *Tax Year. For example, the period from April 1, 2026, to March 31, 2027, is now simply referred to as *Tax Year 2026-27.

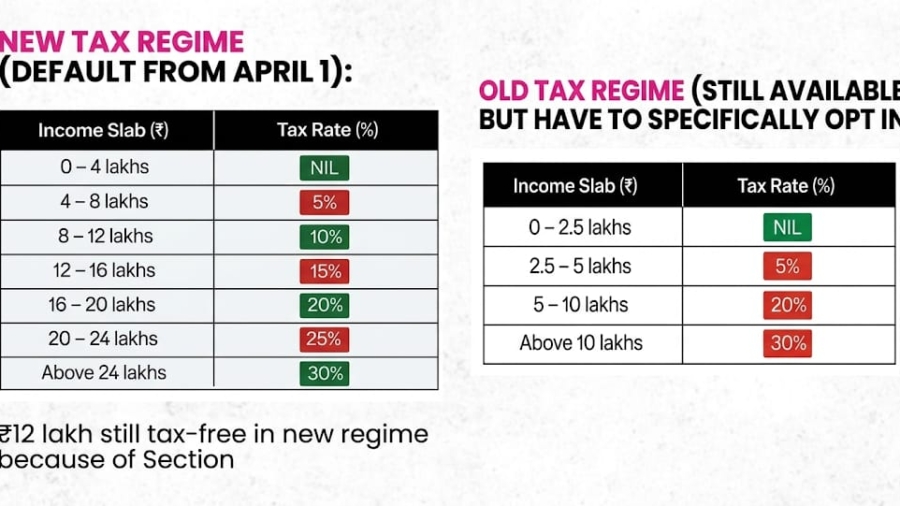

2. Updated Tax Slabs (New Regime)

The New Tax Regime remains the default choice. If you want to use the Old Regime to claim deductions like 80C or HRA, you must specifically opt-in each year.

| Income Slab (₹) | Tax Rate (%) |

|---|---|

| 0 – 4 Lakhs | NIL |

| 4 – 8 Lakhs | 5% |

| 8 – 12 Lakhs | 10% |

| 12 – 16 Lakhs | 15% |

| 16 – 20 Lakhs | 20% |

| 20 – 24 Lakhs | 25% |

| Above 24 Lakhs | 30% |

Note: Under Section 87A, the rebate has been enhanced so that individuals with a taxable income up to ₹12 Lakhs pay zero tax in the New Regime.

3. Key Policy & Deduction Changes

- Standard Deduction: For salaried individuals and pensioners, the standard deduction in the New Regime has been maintained at ₹75,000.

- HRA Exemption Expansion: The 50% HRA exemption (previously limited to the four main metros) now includes Bengaluru, Pune, Hyderabad, and Ahmedabad.

- Increased Perquisite Limits:

- Children’s Education Allowance: Increased from ₹100/month to ₹3,000/month per child.

- Hostel Allowance: Increased from ₹300/month to ₹9,000/month per child.

- Tax-Free Meals: The limit for meal vouchers/vessel meals has risen from ₹50 to ₹200 per meal.

- Dividend Income: You can no longer claim a deduction for interest expenses incurred to earn dividend income.

- Capital Gains & Buybacks: Share buybacks are now taxed as Capital Gains in the hands of shareholders, rather than being taxed as dividends at the company level.

4. Compliance & Filing

- ITR Deadlines: The deadline for filing ITR-3 (Business/Profession) and ITR-4 (Presumptive) has been moved to August 31.

- Revised Returns: You now have up to 12 months from the end of the tax year to file a revised return (increased from 9 months).

- Stock Market (STT): Securities Transaction Tax has increased—Futures moved from 0.02% to *0.05%, and Options from 0.1% to *0.15%.